Dr. Djordje Zivkovic

Partner

Dr. Djordje Zivkovic

Partner

Dr. Djordje Zivkovic brings a robust background in strategy and finance, grounded in academic excellence and practical consulting experience. As a postdoctoral researcher at leading institutions such as the University of St. Gallen and the University of Liechtenstein, he applies analytical thinking and strategic foresight to the evolving intersection of strategy, innovation, and finance – among other areas, in the context of factor-based investing and modern asset management. His professional experience includes strategic consulting and financial advisory, where he leveraged financial analysis to support the development of data-informed strategies and decision-making approaches for corporate clients. He holds a doctorate (summa cum laude) in Business Economics and a Master of Arts in Accounting and Finance. Recognized for his academic achievements and data-driven approach, he has been awarded for outstanding research receiving the Best Dissertation Award from the Government of Liechtenstein and being selected to participate in the prestigious Lindau Nobel Laureate Meeting in Economic Sciences. As a passionate chess player and multiple-time Munich youth champion, he also enjoys football and tennis- balancing intellectual rigor with athletic discipline.

Modern portfolio management demands more than intuition and traditional metrics. As financial markets become increasingly complex and interconnected, sophisticated analytical frameworks have emerged as essential tools for generating consistent alpha. Averdas stands at the forefront of this evolution, employing scientifically validated analytics to deliver the next generation of factor investing. Our investment philosophy centers on productivity gains as the primary driver of economic growth and investor returns. Rather than relying on conventional linear models that oversimplify market dynamics, we harness the power of Data Envelopment Analysis (DEA) to construct optimal portfolios through empirically derived productivity frontiers. This approach enables us to capture non-linear market relationships and identify superior investment opportunities across varying macroeconomic cycles.

The following analysis explores how our data-driven methodology addresses the fundamental limitations of traditional asset management approaches, providing institutional investors with a more sophisticated framework for navigating 21st-century market challenges.

Averdas' Data-Driven Investment Philosophy

At the core of our investment strategy lies a commitment to scientifically rigorous analytics that transcend conventional factor exposure models. Our philosophy recognizes that sustainable investment performance requires a deep understanding of productivity dynamics and their evolution across different market environments. Unlike traditional asset managers who rely heavily on static factor loadings, our approach acknowledges that financial markets exhibit complex, adaptive behaviors that cannot be captured through linear relationships alone. We focus specifically on productivity gains as the fundamental driver of long-term value creation, recognizing that companies and portfolios demonstrating superior productive efficiency are more likely to generate consistent alpha over extended periods.

This productivity-centric approach enables us to identify investment opportunities that remain robust across varying macroeconomic conditions. By analyzing how different assets and factor combinations perform relative to empirically derived efficiency frontiers, we construct portfolios that optimize risk-adjusted returns while maintaining adaptability to changing market dynamics. Our scientifically validated methodology provides institutional investors with a systematic framework for factor selection and portfolio construction that goes beyond traditional risk-return optimization models.

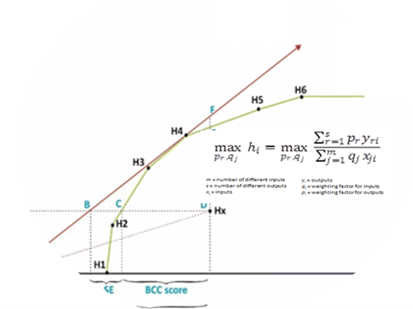

Data Envelopment Analysis (DEA): The Foundation

Data Envelopment Analysis serves as the quantitative backbone of our investment process, providing a mathematically rigorous method for evaluating portfolio efficiency relative to empirically derived productivity frontiers. Originally developed by Banker, Charnes, and Cooper in 1984, DEA offers a non-parametric approach to performance measurement that avoids the restrictive assumptions inherent in traditional linear models.

The DEA framework constructs productivity frontiers by identifying the most efficient combinations of inputs and outputs within a given dataset. In our investment context, this translates to identifying portfolios that achieve optimal risk-adjusted returns relative to their peer universe. Unlike conventional benchmarking approaches that rely on simple return comparisons, DEA evaluates performance across multiple dimensions simultaneously. This multidimensional analysis capability proves particularly valuable when assessing complex investment strategies that may exhibit varying performance characteristics across different market conditions. The DEA approach enables us to identify portfolios that consistently operate near the efficiency frontier, indicating superior management of risk-return trade-offs.

The non-parametric nature of DEA means that our analysis does not impose predetermined functional forms on the relationship between risk and return, allowing for more flexible and accurate representation of actual market dynamics.

Incorporating Future Productivity

While DEA traditionally relies on historical data for frontier construction, our enhanced methodology incorporates forward-looking productivity assessments to ensure comprehensive investment decision-making. This evolution addresses a critical limitation of purely backward-looking analytical frameworks that may miss emerging opportunities or evolving market dynamics. Our quantitative model extends beyond historical performance analysis by evaluating how productivity characteristics may develop under different future scenarios. This approach balances the empirical rigor of historical data with the strategic necessity of forward-looking investment positioning.

The integration of future productivity considerations enables our portfolios to capture both established performance patterns and emerging alpha-generating opportunities. By analyzing productivity trends and their potential evolution, we can identify investments positioned to benefit from structural changes in their operating environments. This temporal dimension adds significant value to the traditional DEA framework, ensuring that our investment decisions reflect both proven historical efficiency and anticipated future performance potential. The result is a more comprehensive and forward-looking approach to portfolio construction that maintains scientific rigor while adapting to evolving market conditions.

Addressing Non-Linearities in Financial Markets

Traditional linear regression models assume constant, proportional relationships between factors and returns—an assumption that significantly oversimplifies the complex dynamics of modern financial markets. Real market environments exhibit feedback loops, behavioral anomalies, and disproportionate reactions that linear methods cannot adequately capture.Our non-linear approach recognizes that improvements in one performance dimension do not necessarily translate to proportional changes in others. For example, reducing portfolio volatility may enhance risk-adjusted returns in certain market conditions while potentially limiting upside capture in others. These nuanced relationships require analytical frameworks capable of modeling complex, context-dependent interactions.

The DEA methodology naturally accommodates these non-linearities by evaluating each portfolio relative to an empirically derived efficiency frontier rather than imposing predetermined functional relationships. This flexibility enables our analysis to capture the full spectrum of risk-return dynamics without forcing artificial linearity assumptions. Recent academic literature has increasingly recognized the importance of non-linear modeling in finance, with approaches including machine learning and non-linear time series analysis gaining prominence. However, these methods are rarely combined with the productivity-based frontier perspective that characterizes our approach, providing Averdas with a distinctive analytical advantage in identifying alpha-generating opportunities.

Detecting Non-Linear Performance Dynamics

The non-linear characteristics of our DEA-based approach enable superior detection of performance patterns that vary across different macroeconomic environments. This capability proves essential for institutional investors seeking consistent alpha generation regardless of prevailing market conditions. Our analysis has demonstrated the ability to isolate companies and portfolios that generate superior outcomes across varying macroeconomic cycles. Through systematic evaluation of performance relative to efficiency frontiers under different economic regimes, we identify investments that maintain their alpha-generating characteristics despite changing external conditions.

Particularly significant is our framework's capacity to identify factors and factor combinations that outperform during periods of heightened market volatility. Traditional models often treat such periods as anomalous, potentially missing valuable investment opportunities that emerge during market stress. Our research paper "A Historical Perspective on Averdas Factor Index Performance across Macroeconomic Cycles" provides empirical evidence of this capability, demonstrating how DEA analysis successfully differentiated performance across rising and falling inflation and growth regimes. This context-dependent performance detection reveals alpha-generating patterns that static models typically overlook.

The ability to identify such dynamic performance characteristics provides institutional investors with significant advantages in portfolio construction and risk management, particularly during transitional market periods when traditional factor relationships may become unstable or asymmetric.

Accounting for Market Anomalies

Rather than treating market shifts and anomalies as noise or unwanted risk factors, our DEA approach incorporates these phenomena as integral components of the investment landscape. This perspective enables a more adaptive and comprehensive investment process that can capitalize on market inefficiencies rather than simply avoiding them. Traditional models often struggle with market anomalies because they violate the underlying assumptions of linear, efficient market behavior. Our non-parametric approach does not impose such restrictive assumptions, allowing for more accurate modeling of actual market dynamics including behavioral biases, structural breaks, and regime changes.

The DEA framework's ability to construct empirically derived efficiency frontiers means that our analysis adapts naturally to changing market conditions. As new data becomes available and market dynamics evolve, the efficiency frontiers adjust accordingly, ensuring that our investment process remains current and relevant. This adaptive characteristic proves particularly valuable during periods of market transition or structural change, when traditional factor relationships may become unreliable. By continuously updating our efficiency frontier analysis, we maintain the ability to identify alpha-generating opportunities even as underlying market dynamics shift.

The forward-looking nature of our approach ensures that portfolio construction decisions reflect both current market realities and anticipated future developments, providing institutional investors with a more robust framework for navigating complex and evolving financial markets.

The Future of Factor Investing

Averdas' data-driven investment approach represents a significant advancement over traditional linear factor models, offering institutional investors a more sophisticated and adaptive framework for alpha generation. Through the systematic application of Data Envelopment Analysis, we provide access to scientifically validated analytics that capture the full complexity of modern financial markets. Our methodology's ability to incorporate non-linear relationships, detect context-dependent performance patterns, and adapt to evolving market conditions positions it as an essential tool for sophisticated institutional investors. The combination of historical empirical rigor with forward-looking productivity analysis ensures comprehensive investment decision-making that addresses both current opportunities and future potential.

For institutional investors seeking to navigate the challenges of 21st-century markets, our approach offers a clear alternative to conventional factor investing methodologies. By embracing the full spectrum of market dynamics rather than oversimplifying them through linear assumptions, we deliver investment solutions that are both scientifically grounded and practically effective. The future of factor investing lies in methodologies that can adapt to complex, evolving market environments while maintaining analytical rigor. Averdas' data-driven approach provides exactly this capability, positioning our clients to achieve superior risk-adjusted returns across varying macroeconomic cycles.