Unlock Higher Returns with Data-Driven Factors on Productivity

Gain actionable insights and outperform benchmarks by leveraging comprehensive analysis of asset, process, resources, and resilience productivity factors.

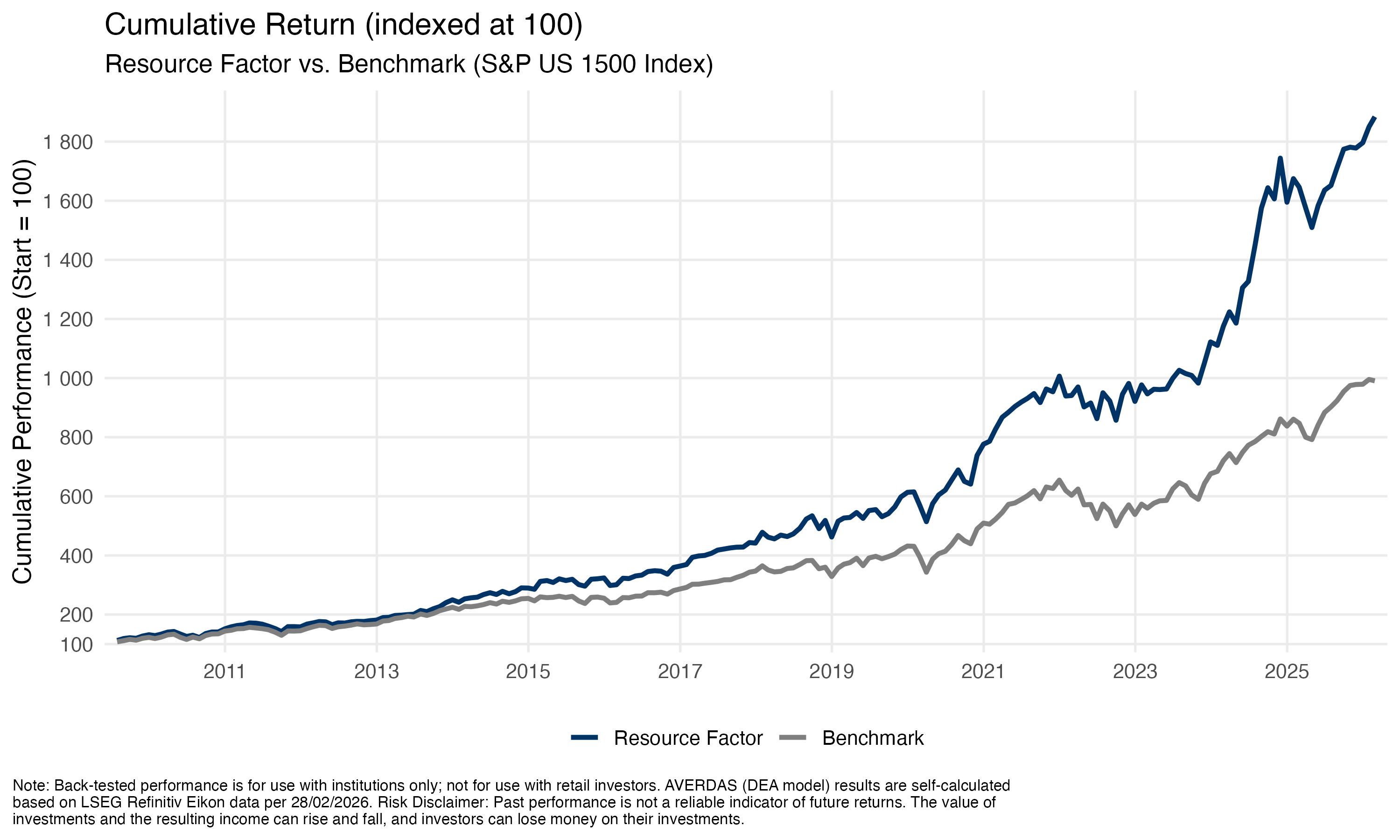

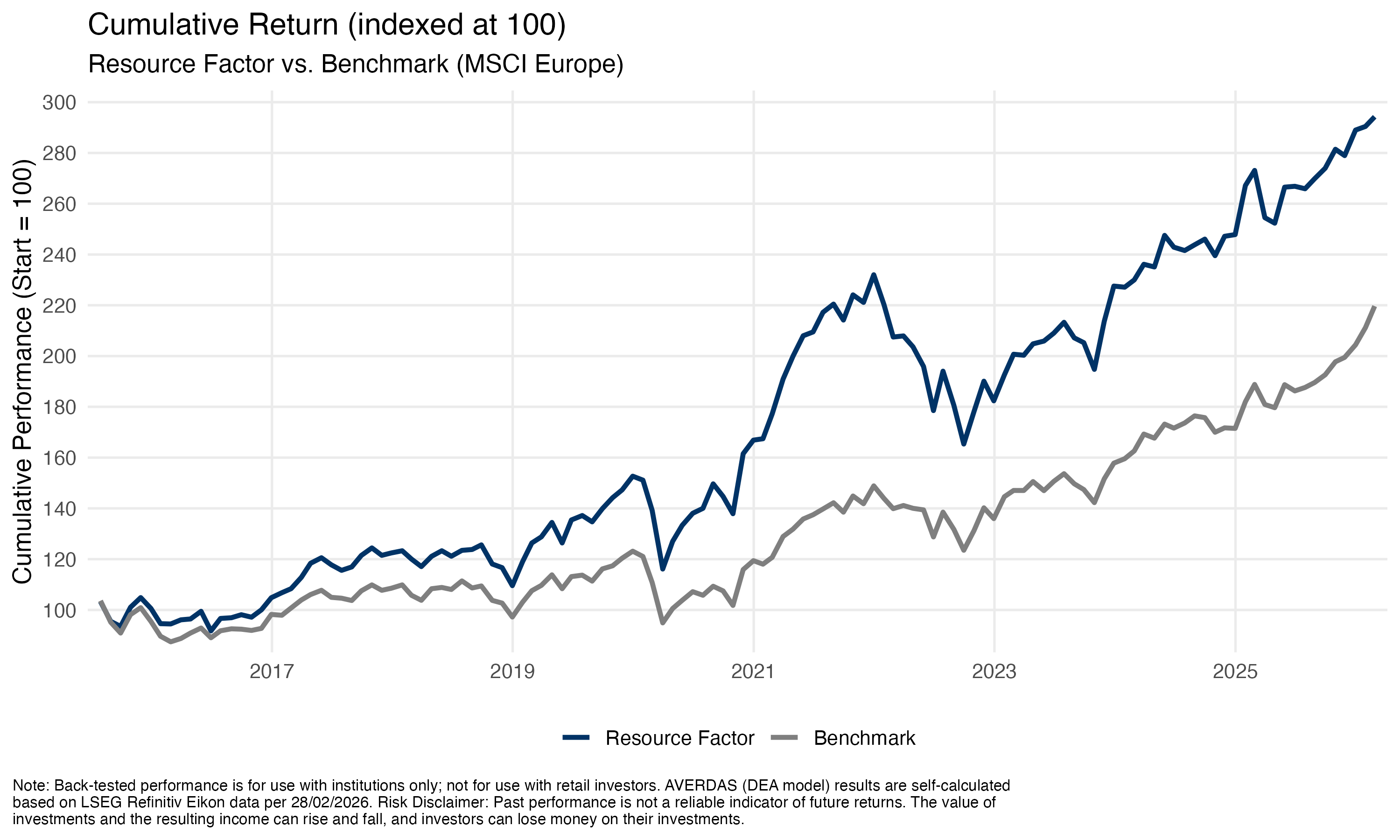

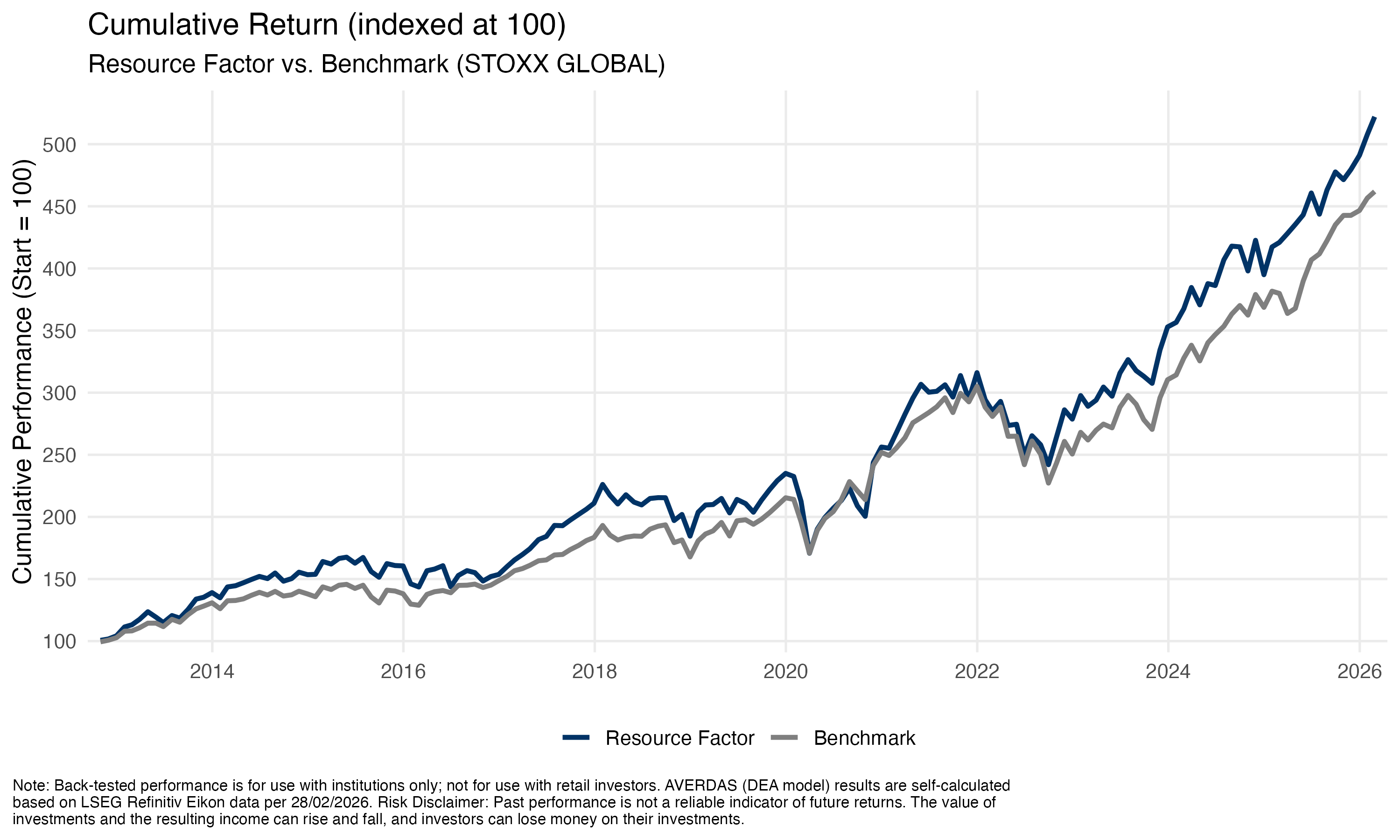

Resource Factor

Make the Business

For sustainable business enabled by efficient use of resources.

How resource factor works?

Resource-efficient stocks tend to outperform resource-inefficient stocks over the long term. This is known as the resource-efficiency-score.

Why they outperform resource-ineffective stocks?

Organizations with a focus on reducing the consumption of resources have better stakeholder scores (i.e., ESG) and higher shareholder values, leading to higher returns.

Make the Business

Resource Factor

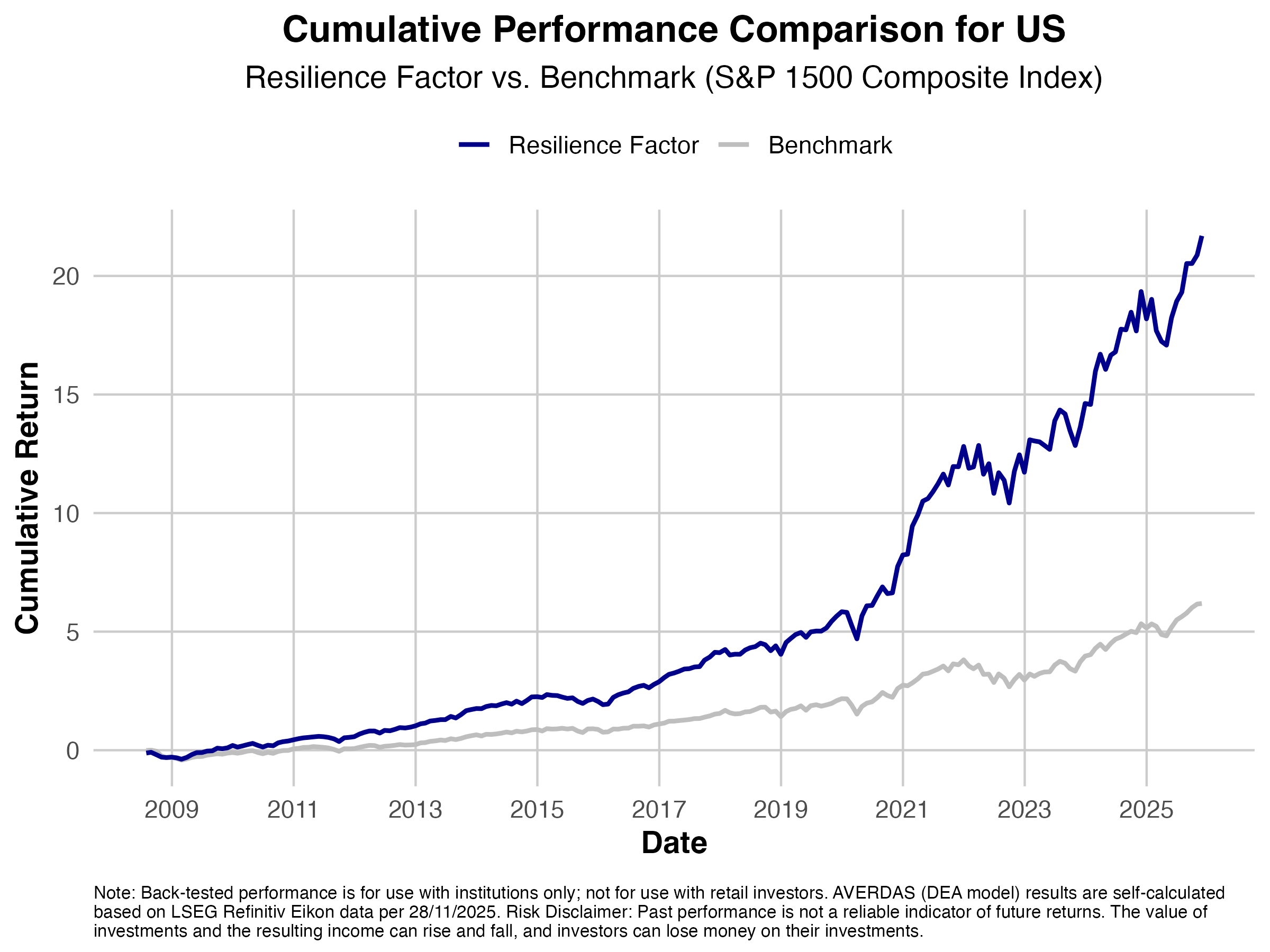

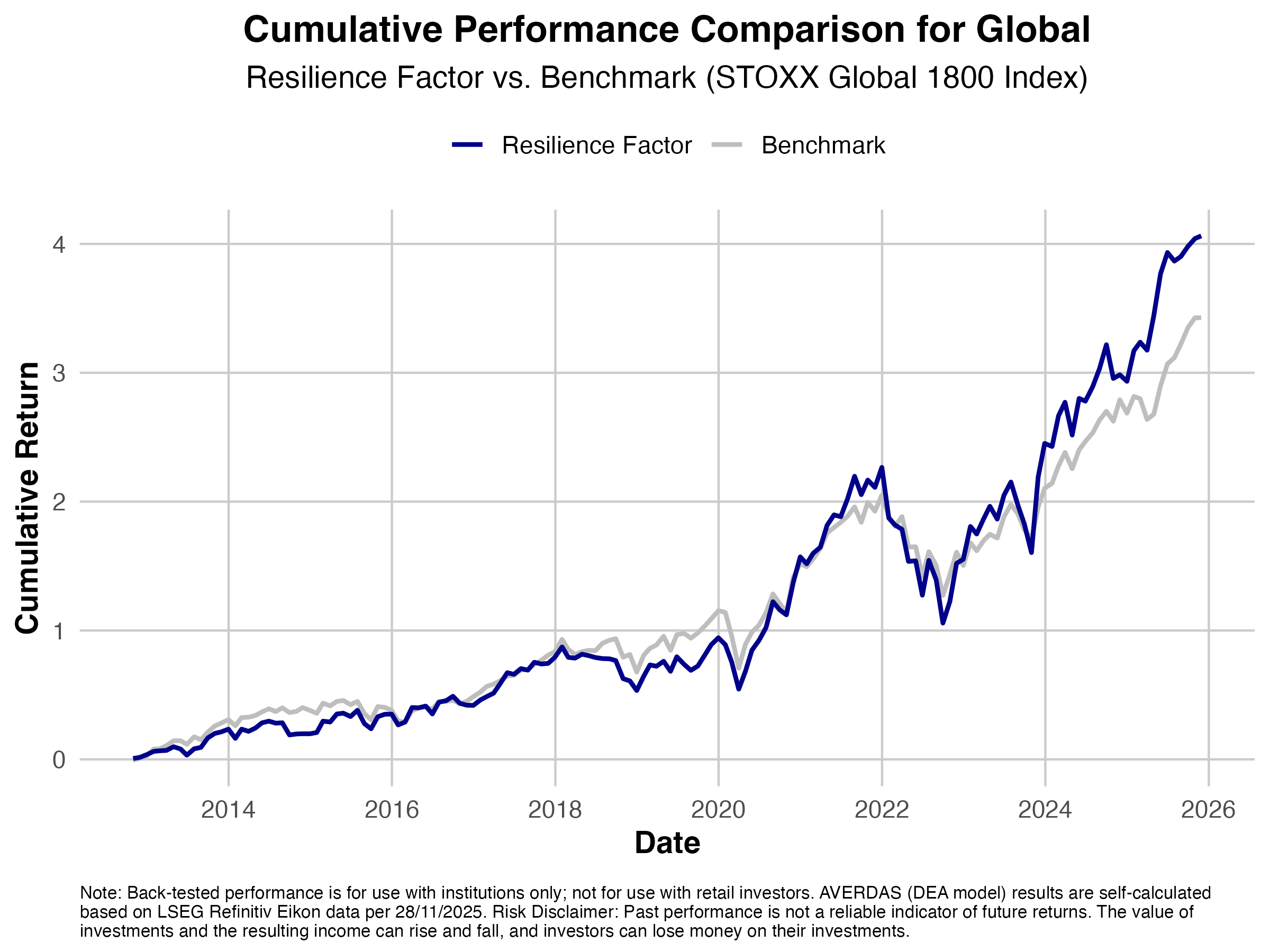

Resilience Factor

Stabilize Business

For stable business enabled by the ability to adapt quickly on a strategic and operational level.

How resilience factor works?

Resilient organizations better cope with disruptive events , “bounce back” faster to a pre disruption state, and “bounce forward” toward unprecedented futures.

Why they outperform resource-ineffective stocks?

Organizations having high resiliency anticipate, adapt and recover better from disruptive events on the systematic, strategic and operational level leading to higher stable returns.

Stabilize the Business

Resilience Factor

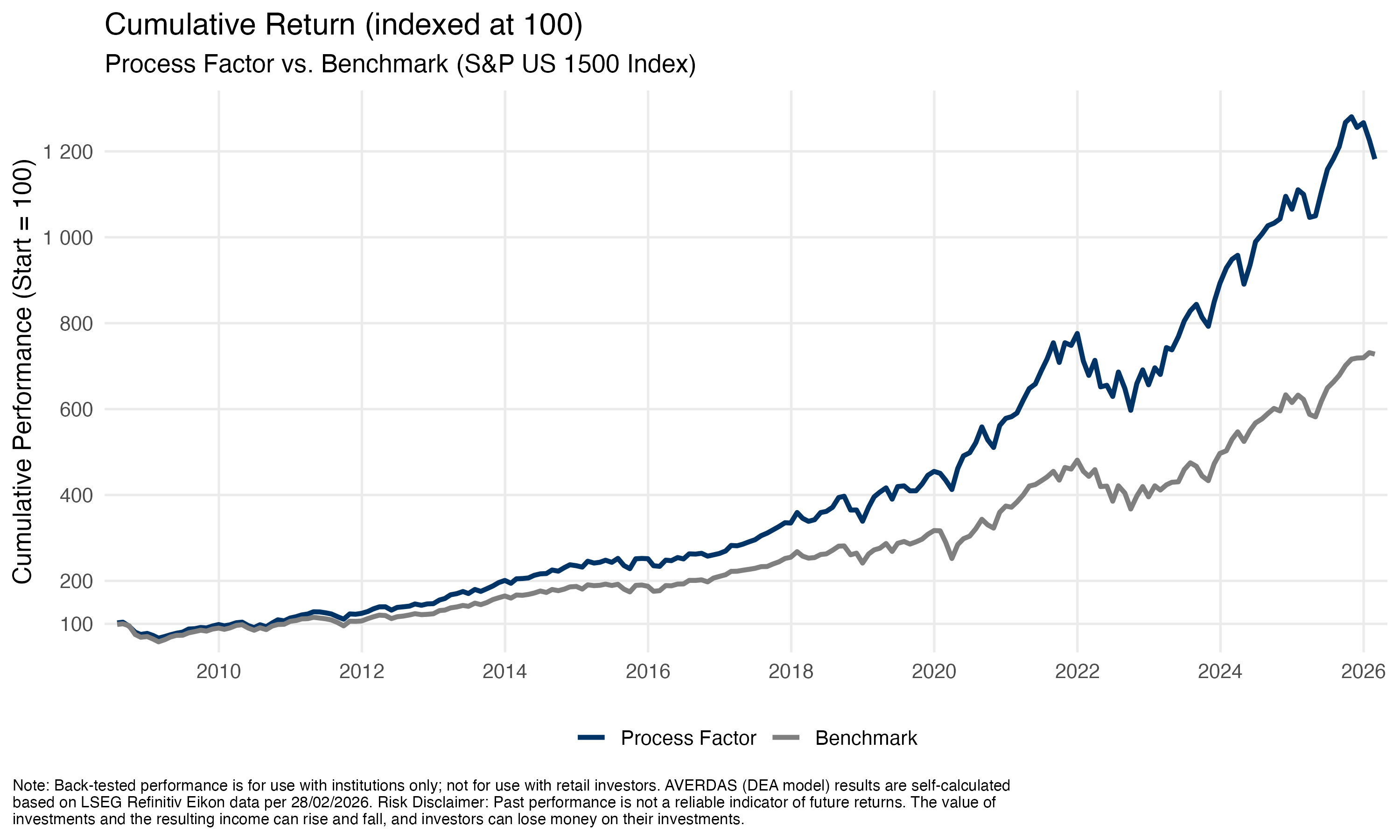

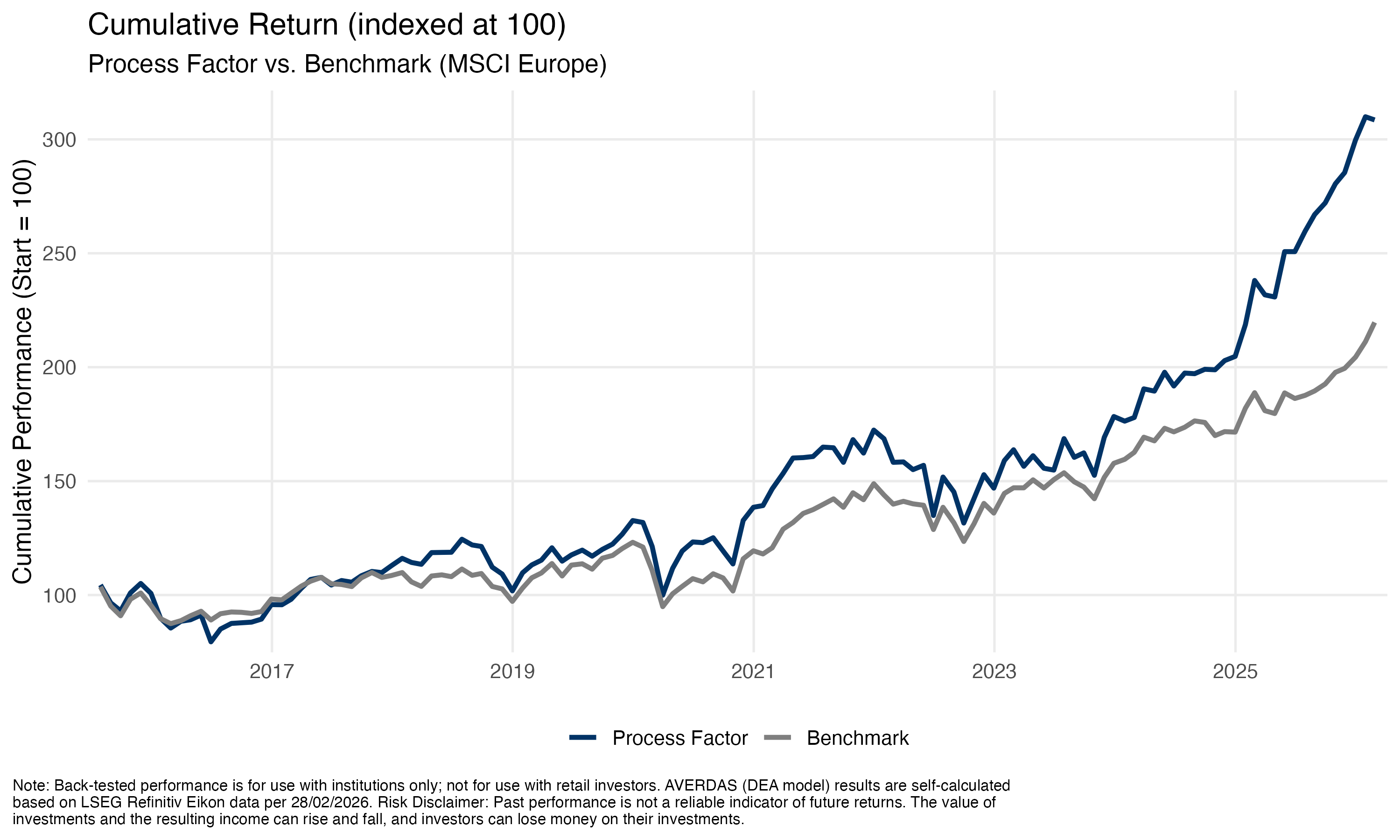

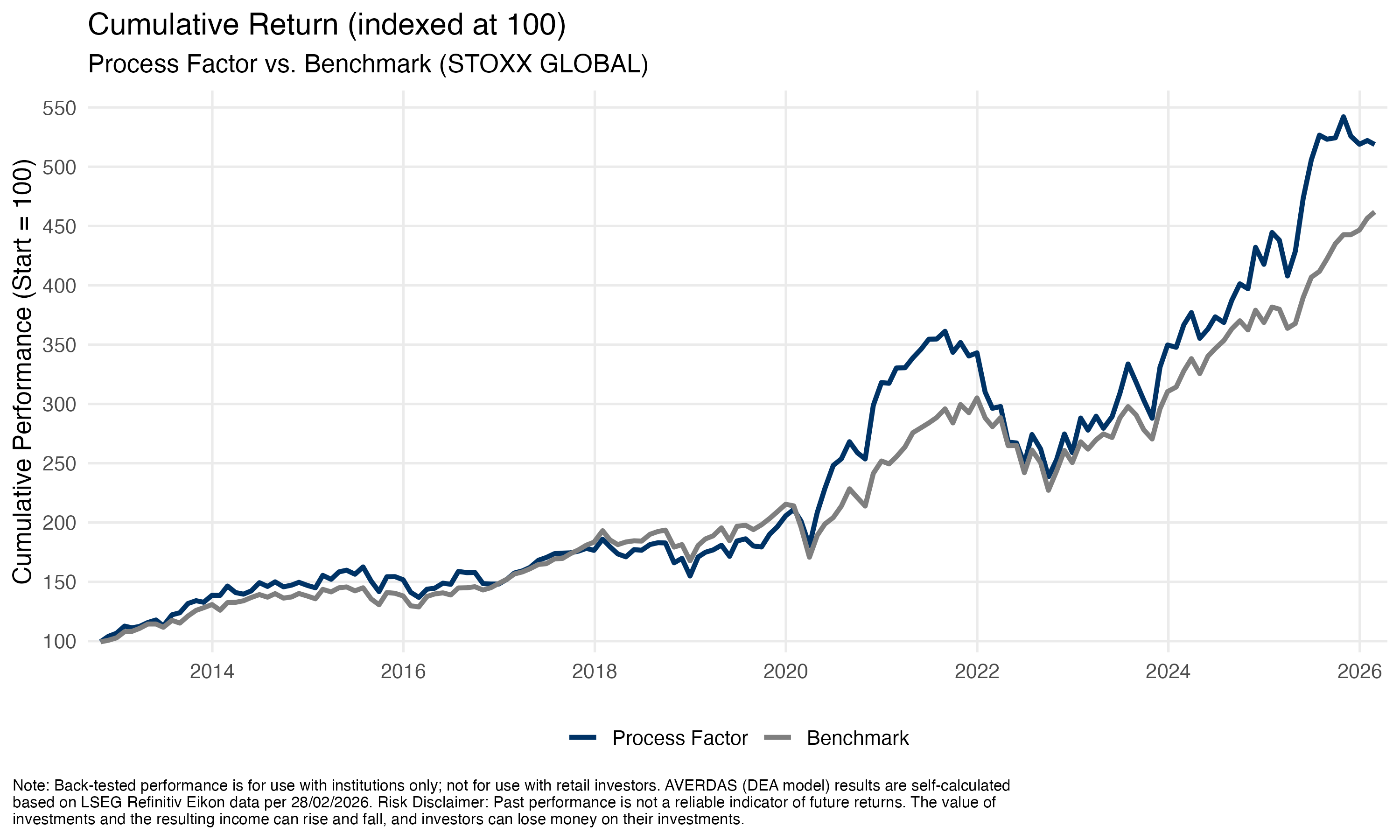

Process Factor

Run the Business

For profitability enabled by efficient use of operational capabilities.

How process factor works?

Process-efficient stocks tend to outperform process-inefficient stocks over the long run. This is known as the operating frontier.

Why they outperform process-ineffective stocks?

Organizations with better dynamic organizational capabilities are more efficient and aligned to the VUCA environment, leading to higher returns.

Run the Business

Process Factor

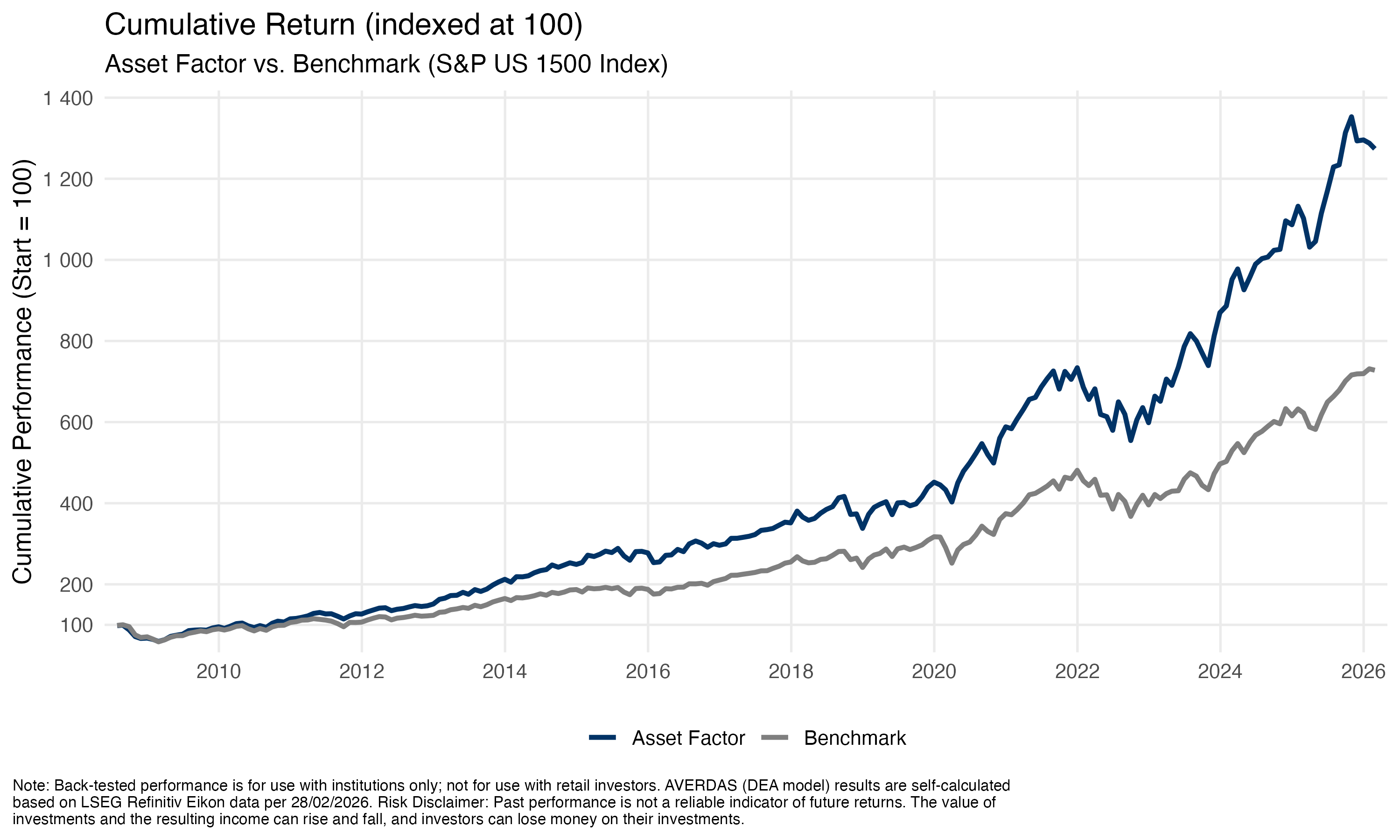

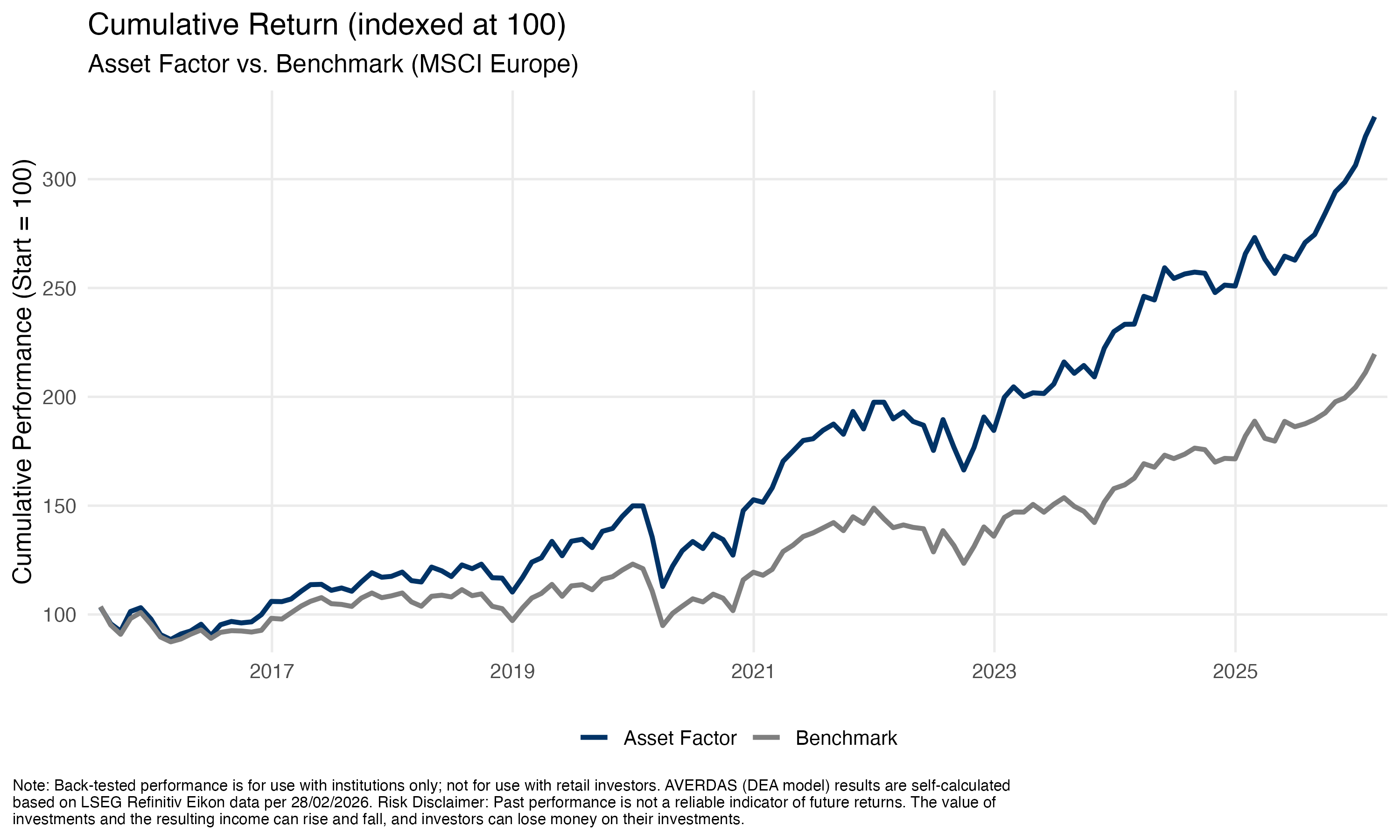

Asset Factor

Build the business

Long term growth enabled by effective use of assets like labor, capital and technologies.

How asset factor works?

Asset-effective stocks tend to outperform asset-ineffective stocks over the long term. This is known as the organizational production possibility frontier.

Why they outperform asset-ineffective stocks?

Organizations that fully utilize their assets will produce a higher quantity of goods more efficiently, leading to higher revenues.

Build the Business

Asset Factor

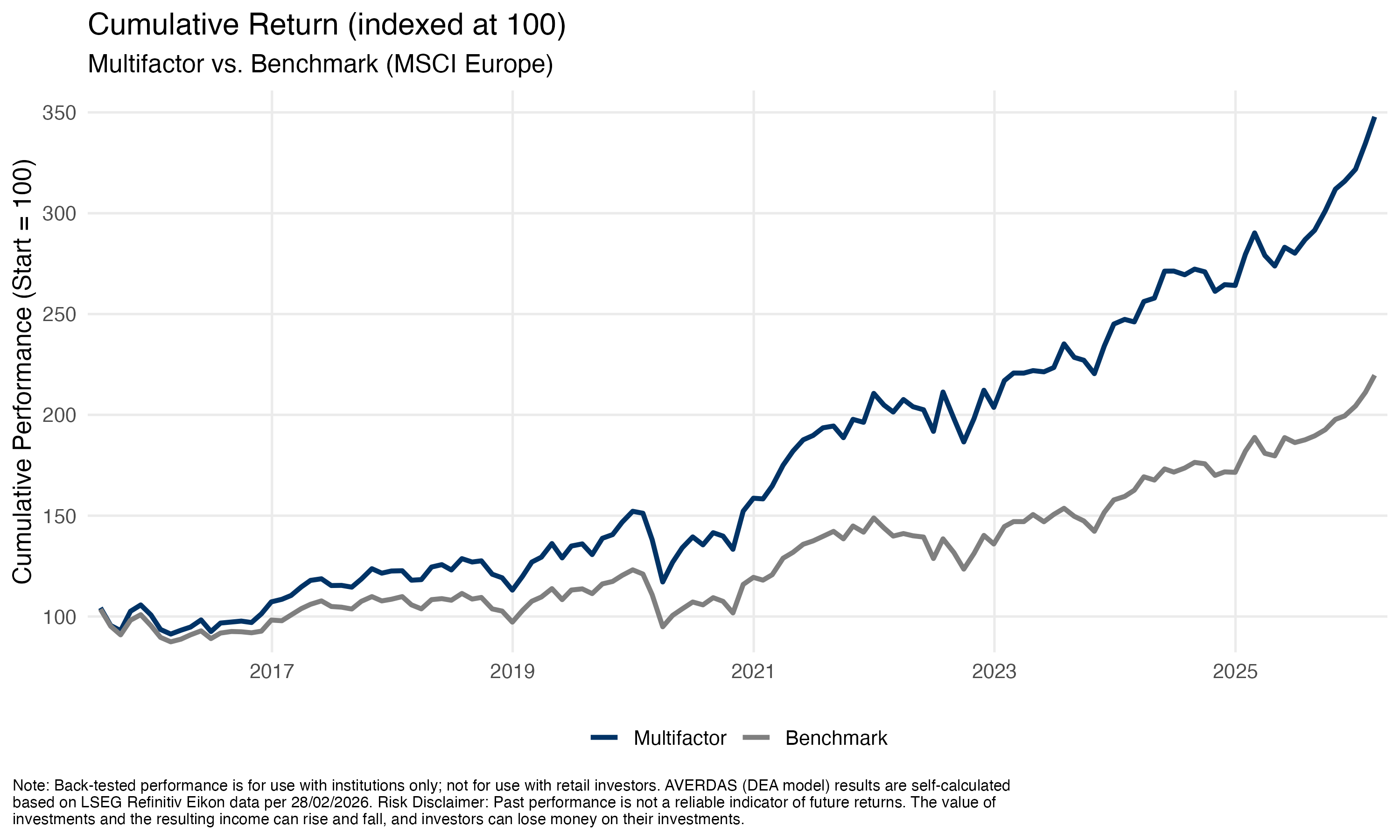

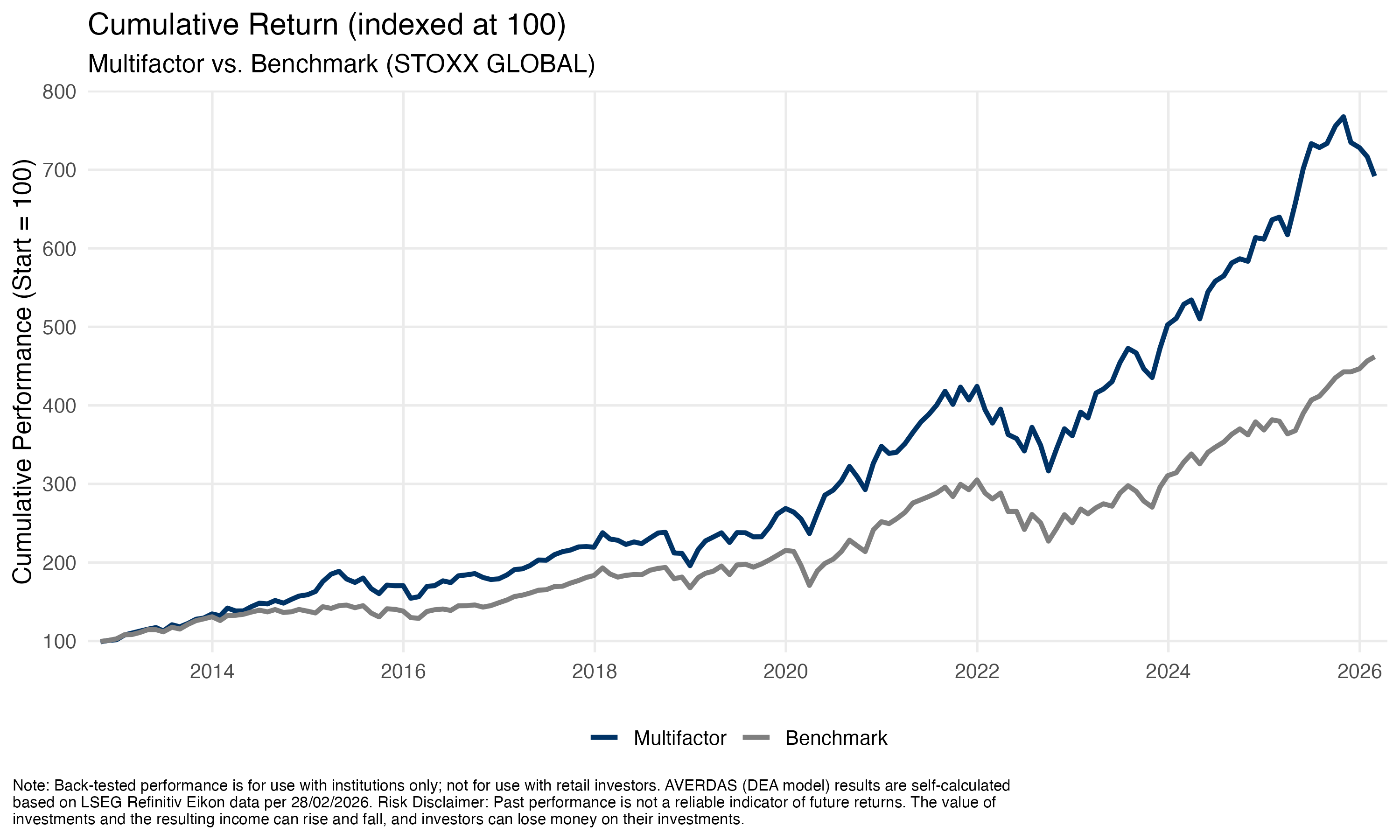

Multi Factor

After calculating each score, a multi-step procedure is applied to identify and select the best performing companies in terms of innovation-productivity, process-productivity, and resiliency. Step 2 builds on Step 1 by selecting the TOP 50 process-efficient companies from the TOP 100 innovation-efficient companies. In step 3 the TOP 20 performing resilient companies are matched with the TOP 50 of the identified companies after step 2. The remaining “spaces” are filled with the TOP 50 companies after step 2. This procedure ensures that the final selection embodies the best performing firms. This approach prevents over-reliance on any single factor while combining the benefits of growth, profitability, and stability.

Multi Factor

Productivity Factors in Investing

Data-Driven Asset Selection

Identification of Non-Linearities and Inefficiencies in the Market

.jpg)

Quantitative and Sophisticated Mathematical Model for Selection

Scientifically Proven Approach

Identification of Robust and Alpha-generating Productivity Leaders

Higher Returns Independent of Macro-Economic Cycles

Sector and Industry Independent

.webp)

Size

Smaller, high-growth companies

Quality

Financially healthy companies

Momentum

Stocks with upward pricetrends

Carry

Income incentive to hold

riskier securities

Value

Stocks discounted relative

to their fundamentals

Minimum volatility

Stable, lower-risk

stocks

Quality

Financially healthy companies

Momentum

Stocks with upward pricetrends

Size

Smaller, high-growth companies

Similar Inputs Lead To Similar Results

Most investors use similar inputs in similar ways, leading to similiar results, including well-known factors such as quality, momentum, growth, value, dividends, low volatility, and size.

We at Averdas use data differently, apply different algorithms for different insights and build our new factors on productivity. With our approach we are able to identify productivity leaders that generate superior returns independent of macro-economic cycles.

Solactive Averdas Indices

Leverage Data-Driven Productivity Insights for Superior Index Performance

Multi-Factor Indices: Combining Factors

While powerful individually, factors also can be used in combination to reflect market outlook and investment objectives. Some common factor combinations include:

Asset + Process

Asset + Resource

Asset + Resilience

Resource + Resilience

Process + Resource

Process + Resilience

Productivty Leaders in Regions

Productivty Leaders in Regions

Averdas Factor Indices Summary

US equities rebounded in July. Productivity Leaders US 500 rose 3.4%, and US 1500 increased 3.0%. The gap between the two universes indicates a wider rebound than the earlier mega-cap rallies. Larger companies remained slightly better. Earnings supported sentiment. Investors became more selective in the AI theme, favoring companies with clearer monetization.

Europe remained strong, with +3.4% growth for Productivity Leaders European Leaders. Financials, energies, industrials, and other value-oriented areas gained from a shift away from technology. Europe's diversification value and good stock/sector selection also helped.

Asia was the only region that declined in July, down 1.1%. Weakness was in semiconductor and artificial intelligence hardware names, following strong gains earlier. A modest decline indicates diversification protection. Asia's outlook depends on the AI investment cycle, offering substantial upside and risk.

Emerging markets ex-Asia was July's best-performing area, growing by +3.8%. Its energy, commodities, and financial sectors all did well. It also has a strong position in the physical infrastructure supporting data center and grid investments. But the region is still quite sensitive to changes in commodity prices, the dollar, and interest rates, meaning there may also be higher volatility.

Overall, in July, the stock market rebounded with gains of +3.3% in the productivity sector. The best-performing regions were EM ex Asia and Europe, followed by the US, while Asia experienced a decline. The market leader expanded beyond the concentrated AI-capex trade, with financials, energy, and cyclical companies also performing well. Investors are now distinguishing between companies with tangible earnings benefits and those dependent on capital spending. July reinforced the value of selectivity and regional diversification.

Source: Averdas Ag. Data as of 31. July 2026. Index performance based on total return (EUR/(USD)

Understanding the Full Scope of Productivity Factors

Asset Factor

Process Factor

Resilience Factor

Resource Factor

Multi-Factor

US

Asset Factor

US

Process Factor US

Resilience Factor US

Resource Factor US

Multi-Factor

US

Europe

Asset Factor Europe

Process Factor Europe

Resilience Factor Europe

Resource Factor Europe

Multi-Factor Europe

Global

Asset Factor Global

Process Factor Global

Resilience Factor Global

Resource Factor Global

Multi-Factor Global

.avif)